Here We Go Here Go Again

- Editors' Option

- REITs

Here We Go Once more

Nov. 27, 2021 x:00 AM ET TCN, EQIX, KKR, BX, DBRG, DLR, AMT, CONE, PINE, SQFT, AHT, SOHO, PEI, GPMT, NYMT, REXR, SVC, VNQ, RQI, RNP, IYR, XLRE, RFI, KBWY, SCHH, NRO, FREL, SRVR, JRS, DRN, USRT, ICF, RWR, DRV, URE, SRS, SEVN, FRI, REK, PSR, BBRE, PPTY, VRAI, IARAX 10 Comments 49 Likes

Summary

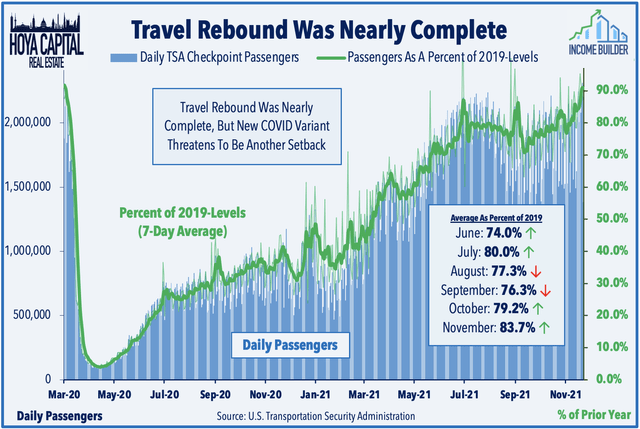

- U.South. equity markets declined on a volatile Thanksgiving calendar week as concerns over an emerging COVID variant triggered a fresh wave of economic restrictions and travel restrictions across Europe and Asia.

- Capping-off the choppy week with the worst single-24-hour interval pass up since Feb, the S&P 500 ended the week lower by ii.1%. Mid-Caps and Pocket-size-Caps dipped over 3% while oil plunged 8%.

- Buoyed by strong performance across the "essential" property sectors - housing, applied science, and logistics - existent estate equities mostly held their basis, just COVID-sensitive sectors were slammed.

- Renewed doubtfulness over the outlook for growth, inflation, and interest rates comes as the BEA reported this week that consumer prices in the The states soared at the fastest charge per unit in 31 years in October.

- Importantly, the U.S. housing industry - which has been a critical source of strength throughout the pandemic - appears to be picking up steam yet again following a summer slowdown.

- This idea was discussed in more than depth with members of my individual investing community, Hoya Capital letter Income Architect. Learn More than »

Finnbarr Webster/Getty Images News

Existent Manor Weekly Outlook

U.Southward. equity markets declined on a volatile Thanksgiving calendar week equally concerns over an emerging COVID variant triggered a fresh wave of economic restrictions and travel restrictions beyond Europe and Asia. The typically uneventful holiday calendar week was annihilation but quiet, first with the renomination of Federal Reserve Chair Jay Powell, continued with a avalanche of economical data that included the highest aggrandizement print in 31 years, and ended with a historic one-24-hour interval commodity sell-off driven by the Omicron COVID variant.

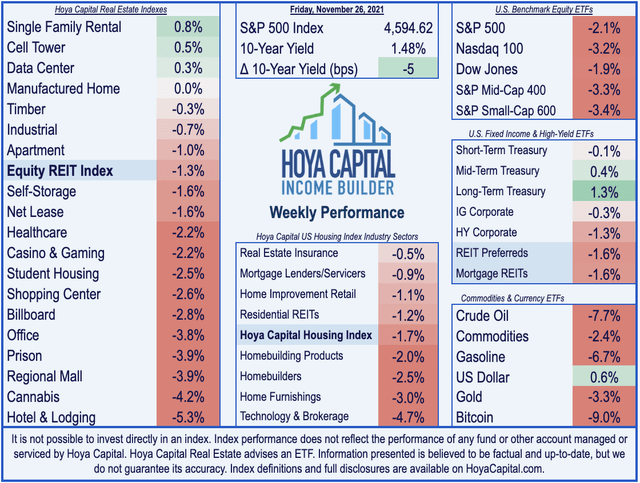

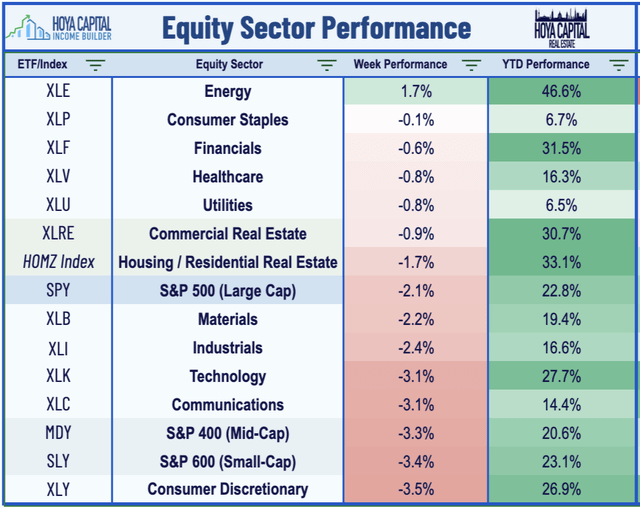

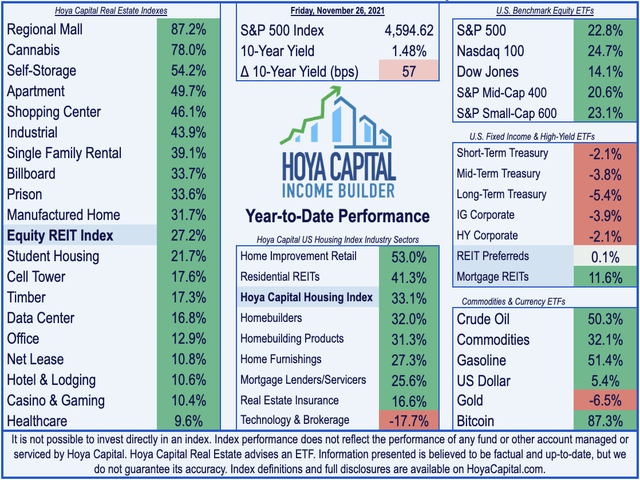

Capping off the inclement week with the worst single-day turn down since February, the S&P 500 (SPY) ended the week lower past ii.1% while the Mid-Cap 400 (MDY) dipped 3.3% and the Modest-Cap 600 (SLY) declined 3.4%. Buoyed by strong performance across the "essential" holding sectors - housing, applied science, and logistics - real estate equities held their ground as the Equity REIT Index ended the week off past one.iii% with 4-of-19 property sectors in positive territory while the Mortgage REIT Index finished lower by 1.6%.

Volatility across equity markets was rather tame compared to the extreme moves seen in global commodity markets equally the combination of COVID concerns and the release of oil from the Strategic Petroleum Reserve sent rough oil prices to their largest i-solar day decline since Apr 2020. Sovereign yields also recorded one of their largest intra-week swings since the pandemic as the 10-Year Treasury Yield soared above i.lxx% following the appear renomination of Fed Chair Powell as investors priced-in college certainty of charge per unit hikes past mid-2022 before plunging to terminate the calendar week below i.l%.

Real Estate Economic Data

Beneath, nosotros recap the most important macroeconomic information points over this past week affecting the residential and commercial real manor marketplace.

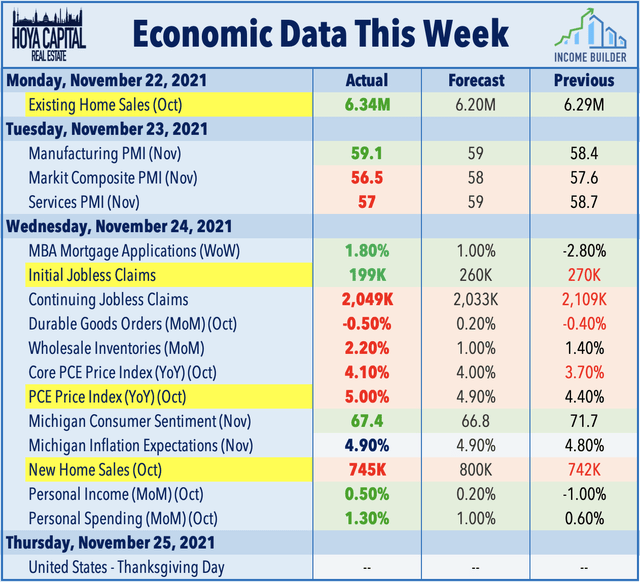

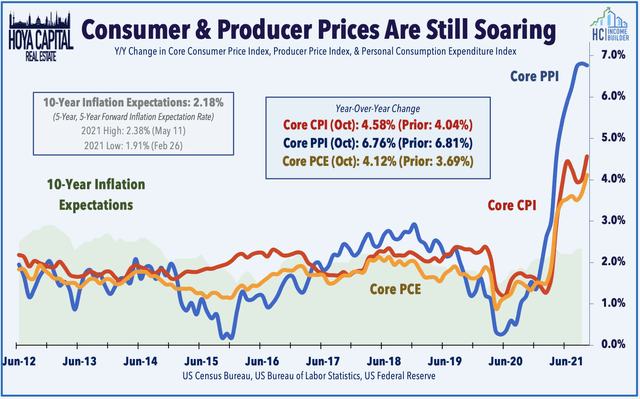

The reimposition of economic restrictions beyond several major economies across Europe and Asia introduces fresh uncertainty over the much-debated outlook for inflation, which comes every bit the BEA reported this week that consumer prices in the US connected surging in Oct with the PCE Cost Alphabetize - the Fed'south "preferred" measure of inflation - rise more than than v% from last year - the highest rate of aggrandizement in more than than three decades. Driving the gains was a 30% yr-over-twelvemonth surge in free energy prices and a five% increase in food prices - problems that have resulted in a celebrated plunge in consumer confidence metrics since late August which remained at decade-lows in this week'southward report from the University of Michigan.

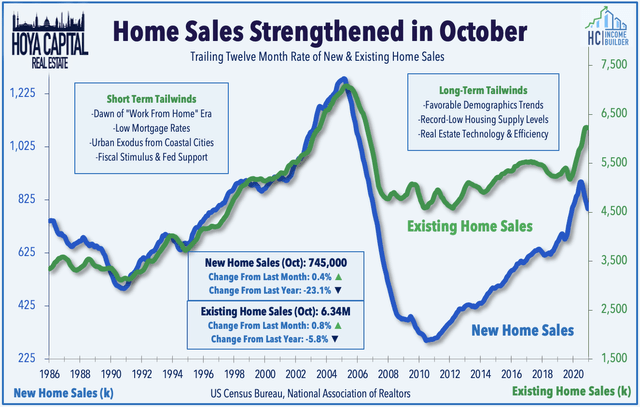

Apart from another historically hot aggrandizement study, the pre-Thanksgiving barrage of economic data was more often than not better-than-expected as weekly Initial Jobless Claims fell sharply while Personal Income and Spending data too topped estimates. Importantly, the U.S. housing industry - which has been a critical source of strength throughout the pandemic - appears to exist picking up steam yet over again following a summer slowdown. New Dwelling Sales rose to the highest level in six months while Existing Sales rose to nine-month highs. Last week, Homebuilder Confidence rose to the highest since May 2020.

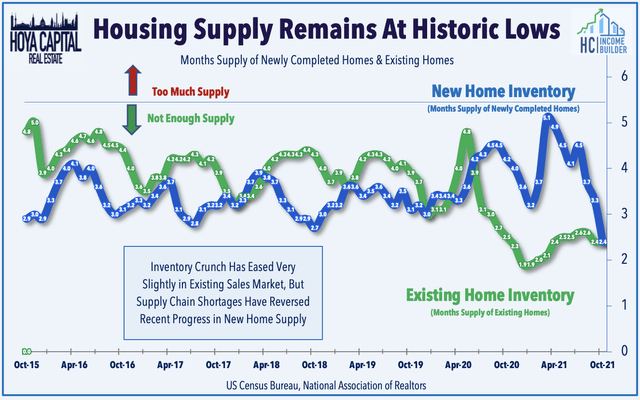

The resilience in home sales comes despite record-low inventory levels with the number of unsold homes declining 12% twelvemonth-over-year to 1.25 one thousand thousand – equivalent to 2.four months of the monthly sales step. Backdrop typically remained on the marketplace for just eighteen days in October, while 82% of homes sold in October 2021 were on the marketplace for less than a calendar month. Naturally, with historically low supply and robust demand, home values and rental rates connected their relentless rise in Oct according to fresh data from ApartmentGuide, which reported that apartment rents for one-sleeping accommodation units are 20% college than concluding twelvemonth while ii-bedroom units have risen 17%.

Equity REIT Week In Review

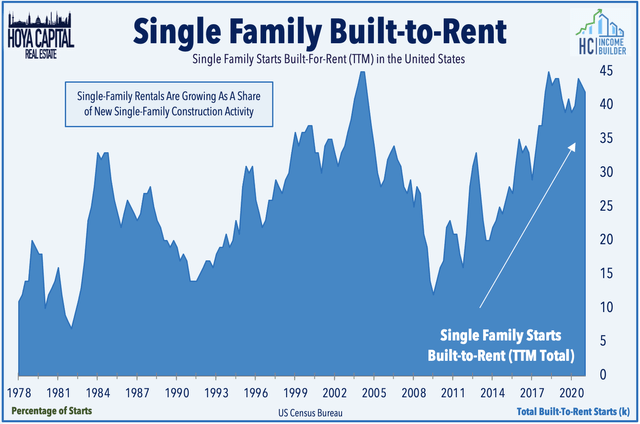

Single-Family Rentals: Speaking of soaring rents, Tricon Residential (TCN) - the fourth-largest owner of unmarried-family homes in the United states of america - announced this week that it now has 3,000 boosted rental units in its structure pipeline through its partnerships with home builders. The communities are under evolution in Tricon's existing single-family rental investment vehicles and Homebuilder Direct JV, and are being built by a number of national and regional homebuilders including four of the top 25 largest homebuilders. We expect SFR REITs and other institutional SFR operators to account for a growing share of new home purchases direct from homebuilders, which should more than offset headwinds on need related to affordability constraints.

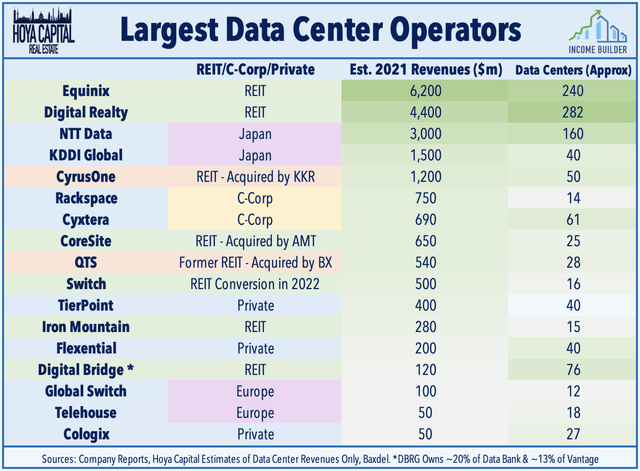

Information Centre: As anticipated, we too saw confirmation that the data eye M&A nail is far from complete. Equinix (EQIX), KKR & Co. (KKR) and Blackstone (BX) are said to be among buyers considering bids for information center operator Global Switch - which operates 13 facilities beyond Europe, Asia, and Commonwealth of australia. Digital Realty (DLR) and DigitalBridge (DBRG) have also reportedly expressed preliminary interest for Global Switch. In Merger Madness, we noted that Digital Realty and Equinix have been uncharacteristically quiet this year on the M&A front end despite sitting on a mountain of "dry pulverisation" as the three smaller data center REITs - CoreSite (COR), CyrusOne (CONE), and QTS Realty - were all scooped-up by competitors.

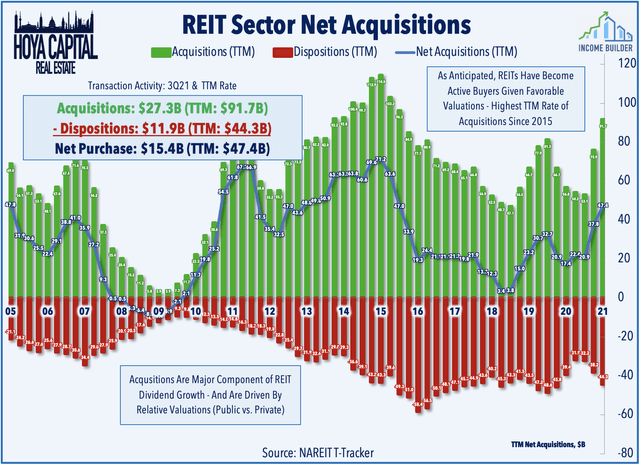

This week, nosotros published Country of the REIT Nation, which discussed how premium valuations have revived the "animal spirits" and sparked a much-needed wave of K&A and IPO activity which has facilitated accretive external growth. With half-dozen completed IPOs and 4 more on the way, 2021 will go down as the most agile year for REIT IPOs since 2013. At the same time, several mega-sized non-traded REITs take scooped upwards public REITs. REITs have caused almost $50B in net avails over the past year - the largest expansion in the asset base since 2015. External growth may exist simply getting started as REIT balance sheets - and access to capital - have never been stronger.

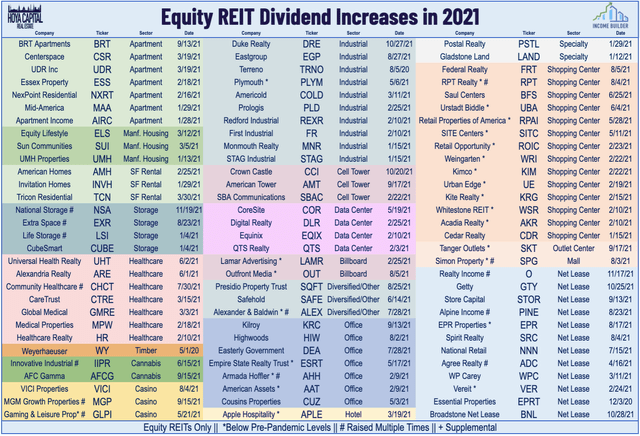

Net Lease: We likewise saw two more REIT dividend increases this week as small-scale-cap net lease REIT Alpine Income Property Trust (Pino) hiked its dividend for the tertiary time this year, while Presidio Holding (SQFT) bumped its dividend for the fourth time this year. In our Country of the REIT Nation study, we discussed how despite the 120 REIT dividend increases this year, the third quarter total dividend payouts were withal twenty% beneath the pre-pandemic third quarter of 2019. With FFO growth significantly outpacing dividend growth, REIT dividend payout ratios remained at just 67% in Q3, indicating that REITs are poised for another big yr of dividend increases in 2022 absent COVID-related setbacks.

Hotels: While residential and applied science REITs provided upside support to the REIT alphabetize this week, in that location was notable weakness across COVID-sensitive REIT sectors - retail, role, and hotels - with 30 equity REITs lower by more than five% on the week including Ashford Hospitality (AHT), which declined most ten% despite announcing that it plans to get current on its accrued preferred dividends later on having deferred cumulative payments over the past six quarters. AHT, which has reported improving operating metrics, was one of a small handful of REITs along with Sotherly Hotels (SOHO) and Pennsylvania REIT (PEI) that however had their preferred dividends suspended.

REIT Preferreds & Capital Raising

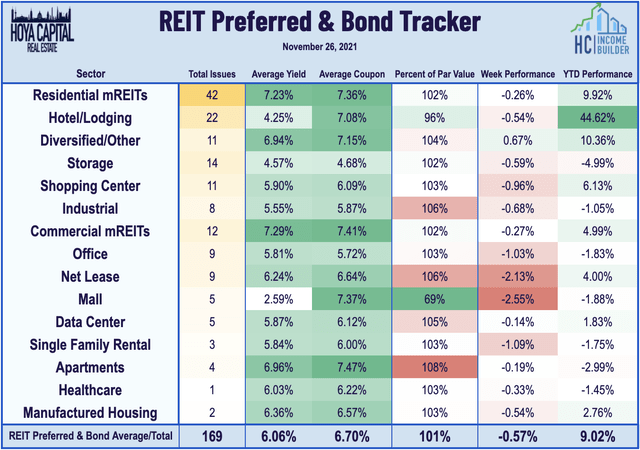

REIT Preferred stocks declined 0.57% this week, on boilerplate, but remain higher by 9.02% on a price-render ground with total returns of roughly 14%. This week, Granite Point Mortgage (GPMT) priced its offset commutation-traded preferred issue - a 7.00% Series A Fixed-to-Floating Charge per unit Cumulative Redeemable Preferred Stock with a $25/share liquidation preference, which information technology will list on the NYSE nether symbol GMPT PrA. Internet proceeds will exist used for the fractional repayment of its 8.00% senior secured term loan facility. Likewise this week, New York Mortgage Trust's (NYMT) new seven.000% Series G Cumulative Redeemable Preferred - began trading on NASDAQ under symbol NYMTZ.

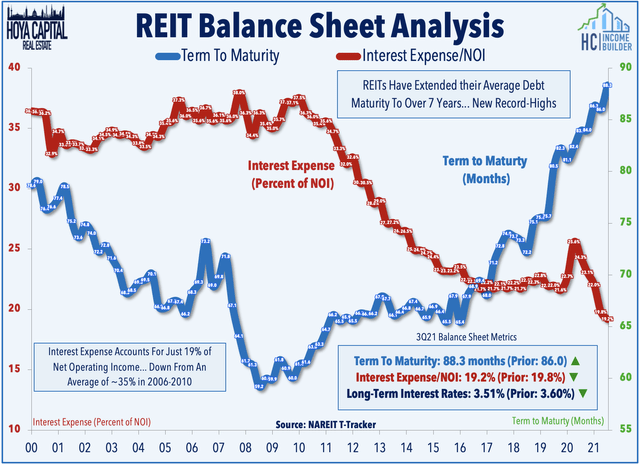

Over in the bond markets this week, Digital Realty announced that information technology extended its existing global revolving credit facility from $2.35 billion to $3.0 billion, and the maturity appointment was extended by three years to January 2027. Elsewhere, S&P affirmed its BBB Long-Term Issuer credit rating for Rexford Industrial (REXR) but lowered its credit rating on Service Properties (SVC) to B+ from BB-. In our State of the REIT Nation report, we analyzed how REITs have used lower rates and plentiful admission to debt capital markets to extend their debt maturities to over vii.3 years and to lower their average long-term interest rate from 3.60% to three.51% over the last quarter.

2021 Performance Cheque-Upward

With merely five weeks remaining in 2021, Disinterestedness REITs are now college by 27.2% this year on a price return ground while Mortgage REITs have gained 11.6%. This compares with the 22.8% accelerate on the South&P 500 and the 20.6% gain on the S&P Mid-Cap 400. Led by the residential and retail holding sectors, all xix REIT sectors are now in positive territory for the year, while on the residential side, seven of 8 sectors in the Hoya Capital Housing Index are likewise higher. At 1.48%, the 10-yr Treasury yield has climbed 57 basis points since the start of the year and is 96 ground points above its all-time endmost low of 0.52% last August, only still 177 footing points beneath its 2018 superlative of 3.25%.

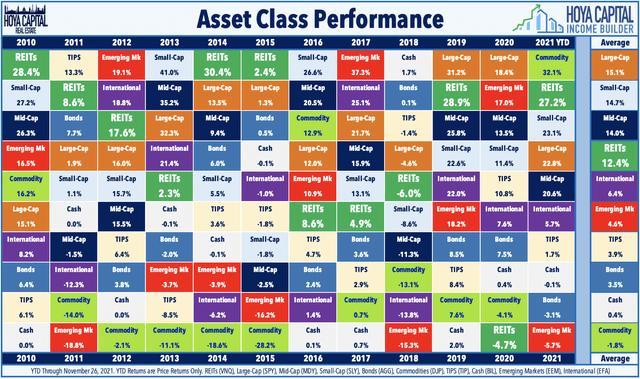

Among the x major asset classes, REITs are once more the second-best performing asset class this year, trailing only the Commodities (DJP) complex. REITs are likewise outpacing Large-Caps and Mid-Caps well as international stocks and bonds. Despite the rough 2020 in which REITs were the worst-performing asset form, REITs are still the fourth best-performing asset classes since the starting time of 2010, producing boilerplate almanac total returns during this time of 12.four%. REITs only slightly lag Small-Cap, Mid-Cap, and Big-Cap equities over this time, producing superior full returns to Bonds (AGG), TIPS (TIP), Commodities, Emerging Markets (EEM), and International (EFA) stocks.

Economical Calendar In The Week Alee

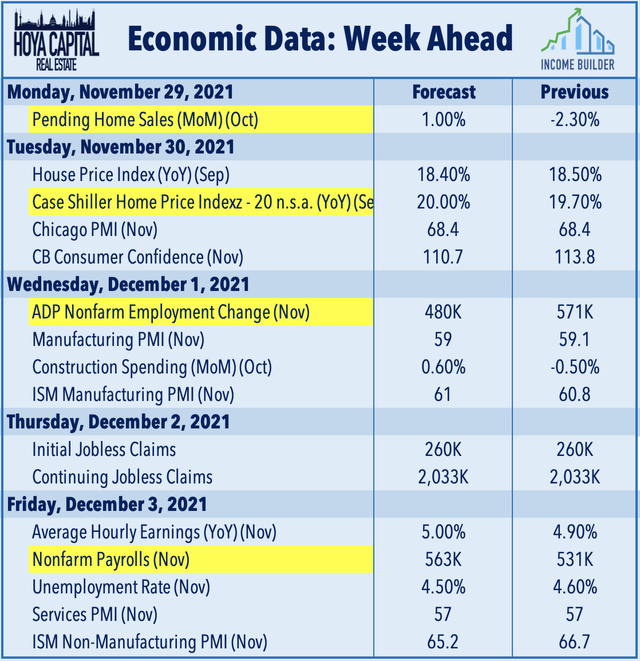

Employment data highlights the economical calendar in the calendar week ahead, headlined past ADP Employment data on Wednesday, Jobless Claims on Thursday, and the BLS Nonfarm Payrolls report on Friday. Economists are looking for job growth of 563K in Nov following last month'southward better-than-expected employment growth of 531K and for the unemployment rate to tick lower to 4.v%. We'll likewise see a flurry of housing data besides with Pending Dwelling house Sales data on Monday, Case Shiller Home Cost Index data on Tuesday, and Construction Spending data on Midweek.

For an in-depth analysis of all real estate sectors, be sure to check out all of our quarterly reports Apartments, Homebuilders, Manufactured Housing, Pupil Housing, Single-Family Rentals, Cell Towers, Casinos, Industrial, Data Center, Malls, Healthcare, Internet Lease, Shopping Centers, Hotels, Billboards, Function, Storage, Timber, Prisons, and Cannabis.

Disclosure: Hoya Upper-case letter Real Manor advises 2 Exchange-Traded Funds listed on the NYSE. In add-on to any long positions listed below, Hoya Uppercase is long all components in the Hoya Upper-case letter Housing 100 Index and in the Hoya Capital High Dividend Yield Index. Index definitions and a complete list of holdings are available on our website.

Introducing Hoya Capital Income Builder

We're excited to announce the launch ofHoya Uppercase Income Builder- the new premier income-focused investing service. Whether your focus is High Yield or Dividend Growth, we've got you covered with actionable investment research and a comprehensive suite of tools and models to help build sustainable portfolio income targeting premium dividend yields of up to 10%. Kickoff your Free Two-Week Trial Today!

Income Architect focuses on real income-producing asset classes that offer the opportunity for diversification, monthly income, capital letter appreciation, and inflation hedging. Members receive complete early on access to our articles along with sectional income-focused model portfolios and trackers.

This article was written past

Build sustainable portfolio income with premium dividend yields up to ten%.

High Yield • Dividend Growth •Income. Visit www.HoyaCapital.com for more information and of import disclosures. Hoya Capital Enquiry is an affiliate of Hoya Upper-case letter Real Manor ("Hoya Capital"), a enquiry-focused Registered Investment Advisor headquartered in Rowayton, Connecticut. Founded with a mission to make real estate more accessible to all investors, Hoya Majuscule specializes in managing institutional and individual portfolios of publicly traded real estate securities, focused on delivering sustainable income, diversification, and attractive full returns.

Collaborating with ETF Monkey, Retired Investor, Gen Alpha, Alex Mansour,The Sunday Investor,and Philip Eric Jonesfor Market service -Hoya Capital Income Architect.

Zero on this site nor any commentary published past Hoya Capital is intended to exist investment, revenue enhancement, or legal advice or an offer to buy or sell securities. Neither the data, nor any opinion, contained on this website or whatsoever published commentary past Hoya Capital constitutes a solicitation or offer past Hoya Capital or its affiliates to buy or sell any securities, nor shall any such security be offered or sold to any person in whatever jurisdiction in which such offer, solicitation, purchase, or auction would be unlawful under the securities laws of such jurisdiction. No representation or warranty is made as to the efficacy of whatever particular strategy or fund, or the actual returns that may be accomplished.

Investing involves hazard. Loss of principal is possible. Investments in real estate companies and/or housing industry companies involve unique risks. Existent estate companies, including REITs, may have limited financial resources, may trade less frequently and in limited book, and may be more volatile than other securities. Many factors may affect existent estate values, including the availability of mortgages and changes in interest rates. Real estate companies are also subject to heavy cash flow dependency, defaults by borrowers, and self-liquidation. The housing industry can be significantly afflicted by the existent manor markets. Compared to large-cap companies, pocket-sized and mid-capitalizations companies may be less stable and their securities may be more volatile and less liquid.

There are also unique risks associated with investing in ETFs. Shares may be bought and sold in the secondary marketplace at market prices and are not individually redeemed from the Fund. Brokerage commissions will reduce returns. Although it is expected that the market price of an ETF volition guess the Fund'south NAV, there may be times when the marketplace price of an ETF is more than than the NAV intra-twenty-four hours (premium) or less than the NAV intra-twenty-four hours (discount) due to supply and demand of the ETF or during periods of market volatility.

Earlier acquiring the shares of an ETF, information technology is your responsibility to read the fund's prospectus. The prospectus to the ETFs in which Hoya Uppercase advises are available at www.HoyaETFs.com.

An investor cannot invest directly in an index. Index functioning does not reflect the deduction of whatever fees, expenses, or taxes. The information and whatever index data presented do not reverberate the performance of any fund or other strategies or accounts managed or serviced by Hoya Capital, and there is no guarantee that investors will feel the type of performance reflected.

Data quoted represents by performance, which is no guarantee of future results. The views and opinions in all published commentary are as of the date of publication and are subject field to change without notice. There is no guarantee that whatsoever historical tendency illustrated will be repeated in the hereafter, and there is no way to predict precisely when such a trend will begin.

Commentary and data are believed to exist accurate, simply we cannot guarantee it's accuracy. We exercise non stand for that information technology is a consummate analysis of all factors and risks. It should not be relied upon as the sole source of suitability for whatever investment. Delight consult with your investment, tax, or legal adviser regarding your individual circumstances before investing.

Decisions based on information independent on this site or whatever commentary published by Hoya Uppercase are the sole responsibility of the reader, and in exchange for using this website or reading any published commentary, the reader agrees to hold Hoya Capital harmless against any claims for damages arising from any decisions that the reader makes based on such information.

Hoya Capital has no business human relationship with any visitor discussed/mentioned. Hoya Capital letter never receives compensation from any company discussed/mentioned. Hoya Majuscule, its affiliates, and/or its clients and/or its employees may concur positions in securities or funds discussed on this website and our published commentary. A complete listing of holdings is available and updated at www.HoyaCapital.com.

Disclosure: I/we have a beneficial long position in the shares of RIET, HOMZ, RIET, DLR, EQIX, GPMT, TCN, NYMT, Pino, REXR either through stock ownership, options, or other derivatives. I wrote this article myself, and information technology expresses my own opinions. I am not receiving bounty for information technology (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this commodity.

Additional disclosure: This is an abridged version of the full report published on Hoya Capital Income Builder on Nov 26th.

Hoya Capital letter Existent Estate ("Hoya Capital") is a research-focused Registered Investment Advisor headquartered in Rowayton, Connecticut. Founded with a mission to make real estate more accessible to all investors, Hoya Capital specializes in managing institutional and individual portfolios of publicly traded real estate securities, focused on delivering sustainable income, diversification, and attractive total returns. A complete word of important disclosures is available on our website (www.HoyaCapital.com) and on Hoya Capital'south Seeking Alpha Profile Page.

Zippo on this site nor any published commentary by Hoya Uppercase is intended to be investment, tax, or legal advice or an offering to purchase or sell securities. Data presented is believed to be factual and up-to-appointment, just we do not guarantee its accuracy and should not exist considered a complete discussion of all factors and risks. Data quoted represents past performance, which is no guarantee of future results. Information technology is non possible to invest directly in an index. Index performance cited in this commentary does non reflect the operation of any fund or other account managed or serviced past Hoya Capital Real Manor.

Investing involves adventure. Loss of main is possible. Investments in companies involved in the real estate and housing industries involve unique risks, as practice investments in ETFs, mutual funds, and other securities. Delight consult with your investment, taxation, or legal adviser regarding your individual circumstances earlier investing. Hoya Capital, its affiliate, and/or its clients and/or its employees may hold positions in securities or funds discussed on this website and our published commentary. A complete list of holdings is available and updated at www.HoyaCapital.com.

Source: https://seekingalpha.com/article/4472114-here-we-go-again

0 Response to "Here We Go Here Go Again"

Post a Comment